Table of Contents

- Introduction

- Why People Ages 25–35 Need Life Insurance

- Why People Ages 36–45 Need Life Insurance

- Why People Ages 46–55 Need Life Insurance

- Case Studies: Life Insurance Needs by Age Group

- Why IUL May Be the Smartest Choice

- IUL vs. Other Life Insurance Options (Comparison Table)

- Expert Quotes on Life Insurance and IUL

- Recent Regulatory and Product Changes Affecting IUL (2024–2025)

- FAQs: Life Insurance and IUL for Ages 25–55

- Checklist: Choosing the Right Life Insurance for Ages 25–55

- Interactive Calculator: Estimate Your IUL Benefits

- Contact Form: Request Your Personalized IUL Illustration

- Conclusion

- References

Introduction

If you’re between the ages of 25 and 55, you’re navigating some of life’s most financially dynamic years. Whether you’re starting a career, building a family, or planning for retirement, life insurance isn’t just for “someone else”—it’s a crucial tool for protecting your loved ones and securing your future. But which policy is right for you? Many experts believe Indexed Universal Life (IUL) insurance offers unique advantages for this age group, blending lifelong protection with flexible, tax-advantaged growth. Let’s break down why life insurance and IUL deserve your attention—no matter where you are on the 25–55 journey.

“Life insurance is not for the people who die, it’s for the people who live.”

— Suze Orman, Personal Finance Expert, The New York Times (2018)[1]

Why People Ages 25–35 Need Life Insurance

Unique Needs and Financial Challenges

- Starting careers and building assets

- Taking on debt (student loans, auto, mortgages)

- Getting married and starting families

- Limited emergency savings

Reasons Life Insurance Matters

- Protects loved ones from debt and funeral costs

- Locks in lower premiums due to younger age and better health

- Builds financial discipline and future planning habits

How IUL Fits

- Flexible premiums accommodate variable income

- Potential for cash value growth tied to market indexes (like the S&P 500)

- Early cash value accumulation can supplement future major expenses

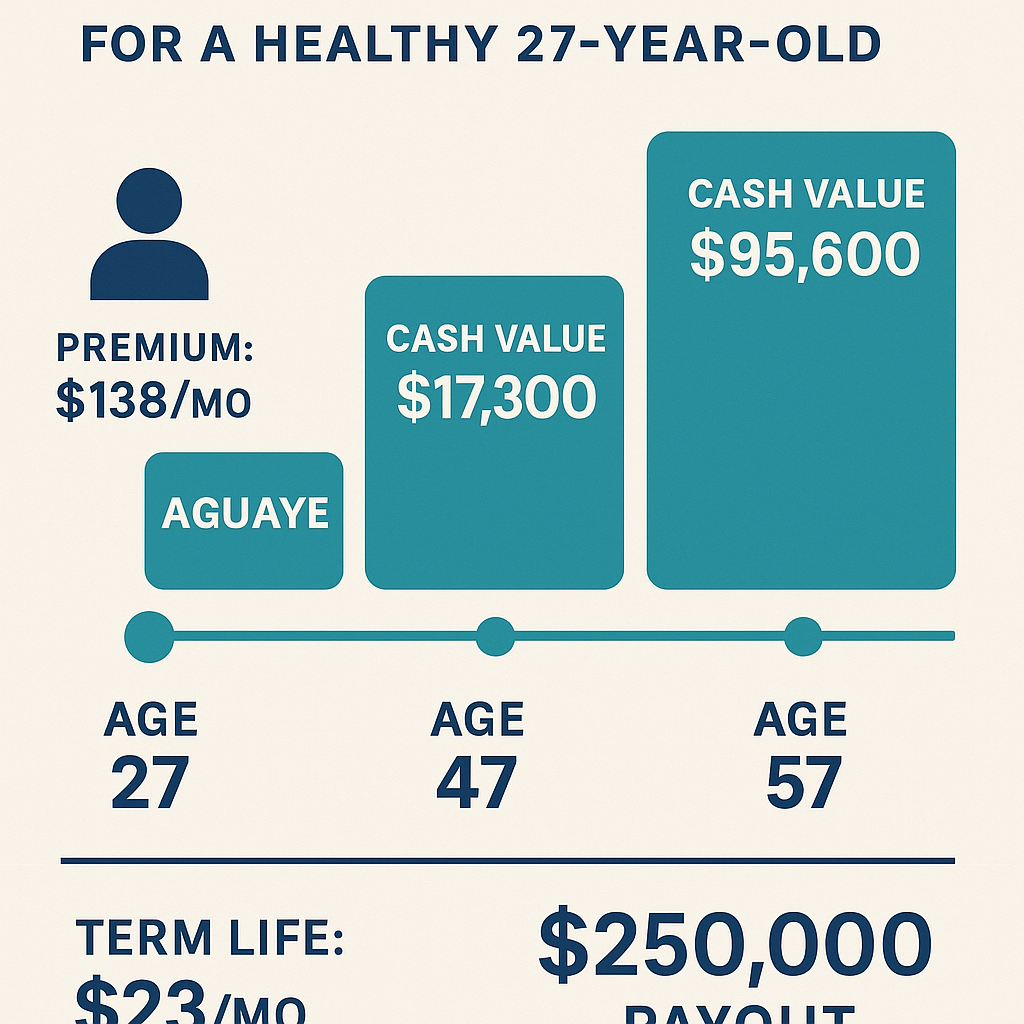

Example: Single 27-Year-Old Professional

Scenario: Emily, age 27, just finished her MBA, has $90,000 in student loans, and is starting her first job.

Life insurance can ensure her debts aren’t passed on to family—and an IUL could begin building cash value now for future use.

Key Elements:

- Entry premium rates for age 27

- Projected cash value growth at different ages

- Comparison to term life cost and payout

Key takeaway: Starting young locks in the lowest rates and maximizes growth potential.

Why People Ages 36–45 Need Life Insurance

Unique Needs and Financial Challenges

- Raising children and increasing expenses

- Mortgage and substantial debts

- Growing income but higher financial responsibilities

- Limited time to recover from unexpected loss

Reasons Life Insurance Matters

- Replaces lost income for dependents

- Pays off mortgage or large debts

- Ensures children’s education and family’s lifestyle

How IUL Fits

- Flexible death benefit to adjust as family grows

- Tax-advantaged cash value can be used for:

- Children’s college tuition

- Emergency medical expenses

- Supplementing retirement savings

Example: 42-Year-Old Parent With Two Kids

Scenario: Mike, 42, has two children (ages 8 and 10) and a $300,000 mortgage.

An IUL can provide lifelong protection, and the cash value could help cover college costs or serve as a retirement supplement.

Key takeaway: Life insurance, especially IUL, offers flexible, long-term protection and savings for growing families.

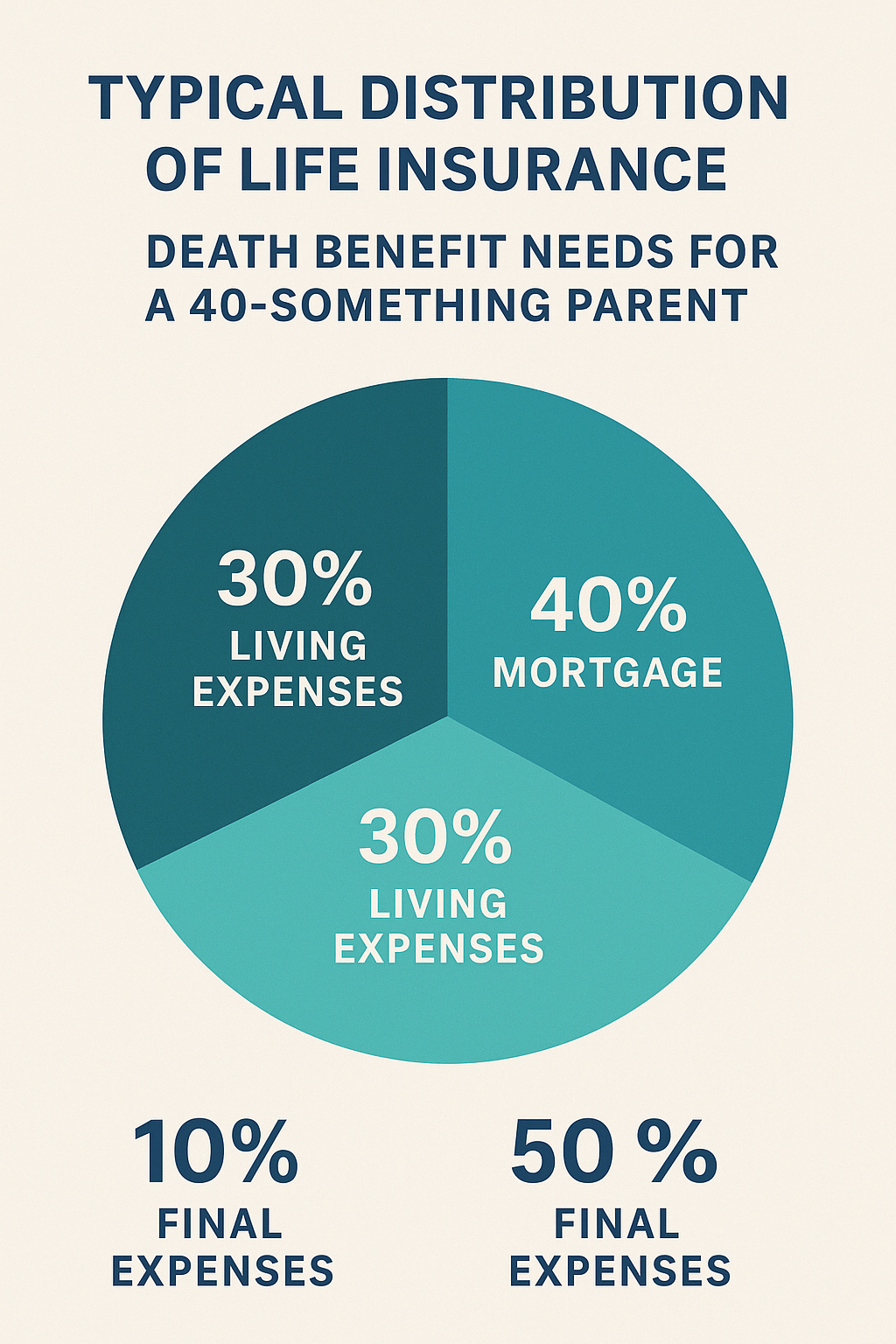

Why People Ages 46–55 Need Life Insurance

Unique Needs and Financial Challenges

- Peak earning years and maximizing retirement savings

- Children nearing college age or becoming independent

- Caring for aging parents

- Preparing for retirement and estate planning

Reasons Life Insurance Matters

- Ensures spouse’s financial security if primary earner passes away

- Helps with estate taxes or legacy planning

- Fills retirement income gaps

- Covers long-term care or medical costs

How IUL Fits

- Catch-up premium flexibility for higher earners

- Potential for tax-free retirement income via policy loans/withdrawals

- Offers a source of funds for long-term care or major expenses

Example: 54-Year-Old Approaching Retirement

Scenario: Lisa, 54, has paid off her mortgage but wants to maximize her retirement income and leave a legacy for grandchildren.

An IUL can provide tax-advantaged growth and a death benefit, addressing both needs.

Key takeaway: IUL can be a powerful tool for retirement planning and wealth transfer.

Case Studies: Life Insurance Needs by Age Group

| Age | Marital/Family Status | Main Concern | Policy Example | IUL Benefit |

|---|---|---|---|---|

| 27 | Single, no kids | Debt, future | $250k IUL | Low premium, cash value grows |

| 41 | Married, 2 kids | Family security | $500k IUL | Income replacement, college funds |

| 53 | Married, empty nest | Retirement, legacy | $1M IUL | Tax-free income, estate planning |

Why IUL May Be the Smartest Choice

What Is Indexed Universal Life (IUL)?

Indexed Universal Life (IUL) insurance is a type of permanent policy offering both a death benefit and a cash value component. The cash value grows based on a stock market index (e.g., S&P 500), but with a floor rate (usually 0–1%) to protect against market downturns[3].

Key Advantages for Ages 25–55

- Lifelong coverage (unlike term, which expires)

- Flexible premiums and death benefits to adapt to life changes

- Tax-deferred cash value growth with market-linked upside (and a floor to prevent losses)

- Potential for tax-free loans/withdrawals in retirement

Potential Drawbacks

- More complex and requires active management

- Higher fees than term or some whole life policies

- Cash value growth not guaranteed—subject to index caps and participation rates

“Indexed universal life insurance offers flexibility and the potential for market-linked growth, making it an attractive option for those planning for long-term financial goals—especially as part of a diversified strategy.”

— David Blanchett, Managing Director, PGIM DC Solutions (2023)[2]

IUL vs. Other Life Insurance Options (Comparison Table)

| Feature | Term Life | Whole Life | Indexed Universal Life (IUL) | Universal Life (UL) |

|---|---|---|---|---|

| Coverage Duration | 10–30 years | Lifetime | Lifetime | Lifetime |

| Premiums | Fixed, lowest | Fixed, higher | Flexible | Flexible |

| Cash Value | None | Guaranteed, fixed | Market-indexed, not guaranteed | Variable/Fixed |

| Flexibility | None | Low | High | Medium |

| Death Benefit | Fixed | Fixed | Flexible, can increase | Flexible |

| Tax Advantages | Death benefit tax-free | Cash value grows tax-deferred | Tax-deferred growth + tax-free loans | Tax-deferred growth |

| Best For | Temporary needs | Conservative savers | Growth-oriented, flexible | Flexibility seekers |

Sources: [SmartAsset][1], [Progressive][2], [Aflac][5]

Expert Quotes on Life Insurance and IUL

“The best time to buy life insurance is when you’re young and healthy—it’s more affordable and can provide greater long-term benefits.”

— Mark Friedlander, Director, Insurance Information Institute (2022)[3]“Indexed universal life can be a useful tool for supplementing retirement income, especially for those who have maxed out other tax-advantaged accounts.”

— Jamie Hopkins, Managing Partner, Wealth Solutions, Carson Group (2022)[4]

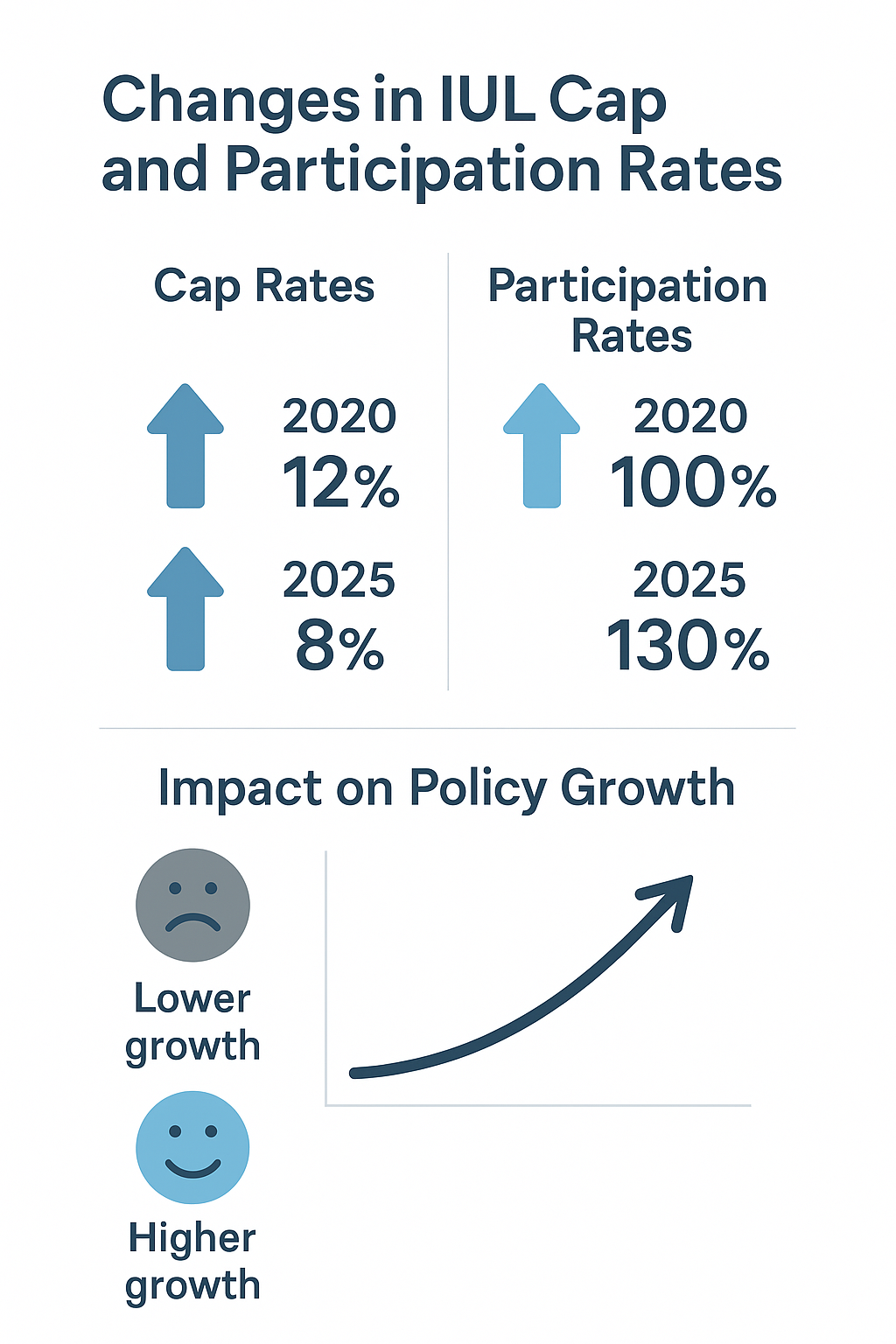

Recent Regulatory and Product Changes Affecting IUL (2024–2025)

- 2024: Many insurers reduced IUL cap rates by 0.5–1% due to ongoing low interest rates, affecting maximum credited interest[5].

- 2025: The IRS reaffirmed tax advantages for life insurance cash value, but new illustrations rules now require clearer disclosure of downside risks and realistic return projections.

- Participation rates (how much of the index gain is credited to the policy) are averaging 45–60% in 2025, down from 60–70% in 2022.

FAQs: Life Insurance and IUL for Ages 25–55

Q: Is IUL right for someone in their 20s or 30s?

A: Yes, because lower premiums and more years to grow cash value can deliver the most benefit[1].

Q: What happens if I can’t pay my IUL premium for a few months?

A: IUL allows you to use accumulated cash value to cover premiums temporarily[2].

Q: How does IUL compare to a 401(k) or IRA for retirement savings?

A: IUL offers tax-deferred growth and tax-free access via policy loans—but typically should supplement, not replace, qualified retirement accounts[3].

Q: Can I lose money in an IUL policy?

A: While you can’t lose principal due to market loss (thanks to the floor), fees and loan interest can erode cash value if not managed[4].

Q: Does IUL make sense if I already have term life insurance at work?

A: Employer coverage often isn’t portable and may be insufficient; IUL provides permanent protection plus savings potential[5].

Checklist: Choosing the Right Life Insurance for Ages 25–55

- Define your main goal: income replacement, wealth accumulation, legacy, or all three

- Calculate your current and future financial obligations (debts, family needs, retirement)

- Review budget and premium affordability

- Compare types of policies (see table above)

- Evaluate cash value and growth potential

- Assess tax advantages for your age and income bracket

- Consult a licensed life insurance professional

Interactive Calculator: Estimate Your IUL Benefits

Enter your age, income, and desired future goal to see estimated IUL premiums, death benefit, and projected cash value at retirement.

Contact Form: Request Your Personalized IUL Illustration

Ready to see how IUL fits your plan?

Fill out our secure form to request a detailed, personalized IUL illustration and speak with a licensed advisor.

- Name, age, contact info

- Current financial goals (drop-down)

- Preferred appointment time

[VIDEO SUGGESTION]

Title: “How an IUL Policy Can Secure Your Future at Any Age 25–55”

Duration: 3–4 minutes

Key Points:

- Real-life testimonials from policyholders in each age group

- Animated walkthrough of IUL features and growth

- Step-by-step guide to getting a personalized illustration

Conclusion

Life insurance is not one-size-fits-all—especially in the dynamic 25–55 age window. With shifting responsibilities, growing families, and retirement on the horizon, protecting your loved ones and your future is essential. Indexed Universal Life (IUL) insurance stands out for its flexibility, lifelong coverage, and unique growth potential. Whether you’re just starting out, raising a family, or planning your legacy, an IUL policy could be the smartest addition to your financial toolkit.

References

[1]: SmartAsset: IUL vs. Whole Life Insurance

[2]: Progressive: Indexed Universal Life vs. Whole Life Insurance

[3]: Western & Southern: IUL vs. Whole Life

[4]: LifeInsure: Battle of the Policies—Indexed Universal Life vs. Whole Life

[5]: Aflac: Term vs. Universal Life Insurance

: Forbes Advisor: 2025 IUL Illustration Rules

: LIMRA: U.S. Individual Life Insurance Sales Trends, Q1 2025

Author Bio:

William Noel, is a licensed financial professional and independent insurance advisor with over 6 years of experience helping individuals and families ages 25–55 build secure financial futures.

Internal Links:

- What Is Indexed Universal Life Insurance? (Guide)

- Life Insurance Needs Calculator

- Case Studies: Real Families Using IUL