(2022)[1]

Table of Contents

- Introduction

- What Is Indexed Universal Life Insurance (IUL)?

- Age-Specific Scenarios: How IUL Addresses Financial Needs Over 55

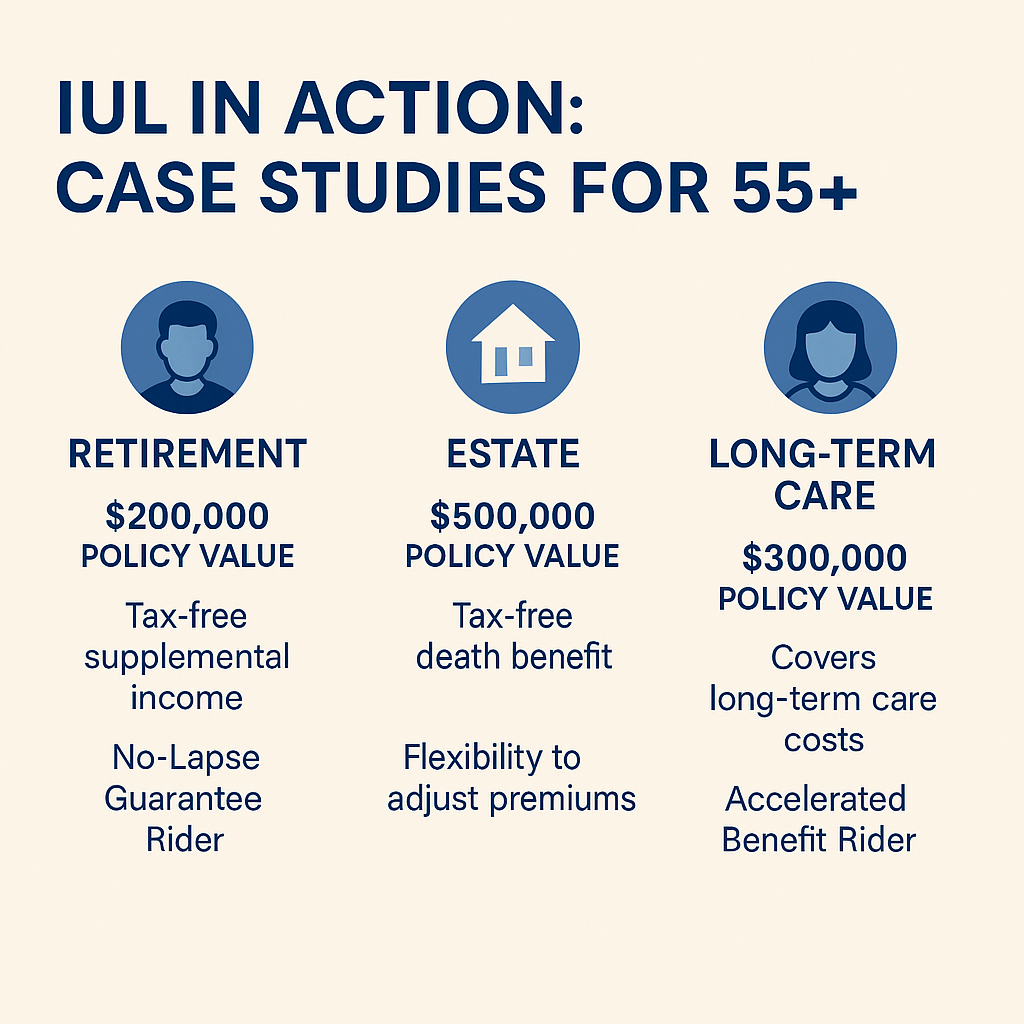

- Case Study 1: Retirement Income Planning

- Case Study 2: Estate Planning

- Case Study 3: Long-Term Care Funding

- Risks and Benefits of IUL for People Over 55

- Indexed Universal Life vs. Other Insurance and Investment Options

- Comparison Table

- Key Features of IUL for People Over 55

- Flexible Premiums and Riders: Managing Changing Financial Needs

- Tax Benefits for Over 55

- Hedging Against Taxes and Market Volatility

- IUL for Over 55: Why This Age Group Is Especially Suited

- Recent Updates: 2024 Tax Law Changes & Product Trends

- Interactive Tools for People Over 55

- Retirement Income & IUL Benefit Calculator

- Suitability Quiz: Is IUL Right for You After 55?

- Frequently Asked Questions (FAQ)

- Conclusion

- References

Introduction

As you approach retirement or settle into your golden years, the financial decisions you make can shape your legacy and security for decades to come. Indexed Universal Life Insurance (IUL) is gaining traction among people over 55 as a dynamic tool for retirement income, tax-advantaged growth, and estate planning. But is it the right fit for you? This comprehensive guide explores how IUL uniquely serves the financial needs of older adults, with real-life scenarios, expert insights, and up-to-date industry statistics.

“The flexibility and tax advantages of indexed universal life insurance make it a powerful asset for retirees seeking both security and growth.” — David McKnight, Author of ‘The Power of Zero’, Financial Planner (2022)[1]

What Is Indexed Universal Life Insurance (IUL)?

Indexed Universal Life Insurance is a type of permanent life insurance that combines a death benefit with a cash value component. This cash value grows based on the performance of a stock market index (like the S&P 500), but with downside protection to shield your savings from market losses[4]. IUL offers:

- Flexible premiums: Adjust payments to match your changing financial circumstances[3][4].

- Tax-deferred cash value growth: Money inside the policy grows without immediate tax consequences[3].

- Tax-free access: Policy loans and withdrawals can be structured to be tax-free, especially in retirement[2][5].

- Customizable riders: Add features like long-term care benefits or accelerated death benefits[3].

Age-Specific Scenarios: How IUL Addresses Financial Needs Over 55

IUL policies are particularly effective for people over 55 who face unique financial challenges: funding retirement, protecting heirs, and preparing for possible healthcare costs.

Case Study 1: Retirement Income Planning

Scenario:

Linda, age 58, wants supplemental income for retirement without risking her nest egg in volatile markets. She invests $2,000/month in an IUL. By age 65, her policy accumulates an estimated $291,000 in cash value and can provide an annual tax-free income of $31,000[1].

“Indexed universal life insurance is one of the few tools that allows for tax-free income distributions in retirement, which is increasingly important as tax rates fluctuate.” — Ed Slott, CPA, IRA Expert, Ed Slott & Company (2021)[2]

Key Takeaways:

- IUL provides a source of tax-free retirement income.

- No required minimum distributions or age penalties, unlike IRAs or 401(k)s[5].

Case Study 2: Estate Planning

Scenario:

James, age 62, wants to leave a substantial legacy for his children while minimizing estate taxes. His IUL policy offers a death benefit of $661,000 at age 65 (for a $2,000/month contribution)[1]. The death benefit passes income-tax-free to his heirs.

Key Takeaways:

- IUL helps transfer wealth efficiently, bypassing probate and reducing estate taxes.

- The death benefit can be customized for specific legacy goals[3].

Case Study 3: Long-Term Care Funding

Scenario:

Mary, age 60, worries about long-term care costs draining her retirement savings. She adds a long-term care rider to her IUL, allowing her to access part of the death benefit for qualifying expenses[3].

Key Takeaways:

- IUL can provide living benefits, including accelerated death benefits for chronic illness or long-term care.

- Riders offer protection against unexpected health costs.

Risks and Benefits of IUL for People Over 55

Benefits:

- Market-linked growth with downside protection (often a 0% floor): Offers upside potential without risk of loss due to market downturns[4].

- Tax-advantaged accumulation and withdrawals: Cash value grows tax-deferred and can be accessed tax-free through policy loans[3][5].

- Flexible premiums: Adjust payments as financial needs change[3].

- Customizable with riders: Add benefits for chronic illness, disability, or long-term care[3].

Risks:

- Costs and fees: IUL policies can have higher fees than term or whole life insurance, affecting cash value growth if not managed[4].

- Policy lapse risk: Insufficient premiums or over-borrowing can cause the policy to lapse, resulting in loss of benefits[3].

- Complexity: Requires careful management and understanding of policy mechanics[5].

- Cap rates: The insurer often sets limits on returns, so you may not receive full market gains[4].

“IULs can be a great fit for some, but they’re not for everyone. Understanding the costs and features is critical, especially for older adults.” — Jamie Hopkins, Managing Partner of Wealth Solutions, Carson Group (2023)[3]

Key Takeaways:

- Evaluate IUL against your risk tolerance, retirement goals, and estate planning needs.

- Work with a qualified financial professional to design the right policy structure.

Indexed Universal Life vs. Other Insurance and Investment Options

For people over 55, comparing IUL to whole life, term life, and annuities reveals distinct advantages and trade-offs.

Comparison Table

| Feature | Indexed Universal Life (IUL) | Whole Life Insurance | Term Life Insurance | Fixed Indexed Annuity |

|---|---|---|---|---|

| Death Benefit | Yes (flexible, adjustable) | Yes (guaranteed) | Yes (fixed, expires) | No |

| Cash Value Growth | Market index-linked, capped | Fixed interest | None | Market index-linked |

| Premium Flexibility | High | Low | Low | Medium |

| Tax-Advantaged Withdrawals | Yes (loans, withdrawals) | Yes (loans, withdrawals) | No | Yes |

| Living Benefit Riders | Available | Limited | Rare | Some |

| Estate Planning Value | High | High | Low | Low |

| Long-Term Care Options | Yes (rider) | Yes (rider) | No | Yes (some products) |

| Market Downside Protection | Yes (0% floor) | Yes | N/A | Yes (0% floor) |

| Age Restrictions | None | None | None | Yes (usually 85 max) |

| Policy Lapse Risk | Moderate (manage carefully) | Low | Low | Low |

Key Takeaways:

- IUL offers unique combinations of flexibility, tax advantages, and living benefits, especially useful for those nearing or in retirement.

Key Features of IUL for People Over 55

- Flexible premium payments: Adjust contributions as your income fluctuates in retirement[3][4].

- Tax-deferred growth and tax-free withdrawals: Mitigate the impact of increasing taxes on retirement income[5].

- Policy loans: Access cash value without triggering taxable events[1][2].

- Customizable riders: Add protection for long-term care, chronic illness, or disability[3].

- Adjustable death benefit: Increase or decrease coverage as needs change[4].

“The ability to borrow against your policy and customize coverage with riders is especially valuable as financial needs evolve in retirement.” — Susan Neely, President & CEO, American Council of Life Insurers (2022)[3]

Key Takeaways:

- IUL adapts to changing financial needs, making it an ideal solution for retirees.

Flexible Premiums and Riders: Managing Changing Financial Needs

As your financial situation evolves after age 55—whether due to retirement, health issues, or shifting priorities—IUL allows you to:

- Increase or decrease premiums within policy limits[3].

- Add riders for long-term care, chronic illness, or disability[3].

- Withdraw or borrow cash value for emergencies or opportunities, with careful management.

Tax Benefits for Over 55

- Tax-deferred growth: Cash value accumulates without current taxes[1][3].

- Tax-free loans and withdrawals: Access policy funds without triggering taxable events[5].

- Income-tax-free death benefit: Beneficiaries receive the death benefit without federal income tax[3].

According to the National Association of Insurance Commissioners (NAIC), life insurance death benefits are generally exempt from federal income tax.

“With rising uncertainty around future tax rates, the tax advantages of IUL are more important than ever for retirees.” — Wade Pfau, Professor of Retirement Income, The American College (2023)[5]

Key Takeaways:

- IUL can provide significant tax shields for retirement income and wealth transfer.

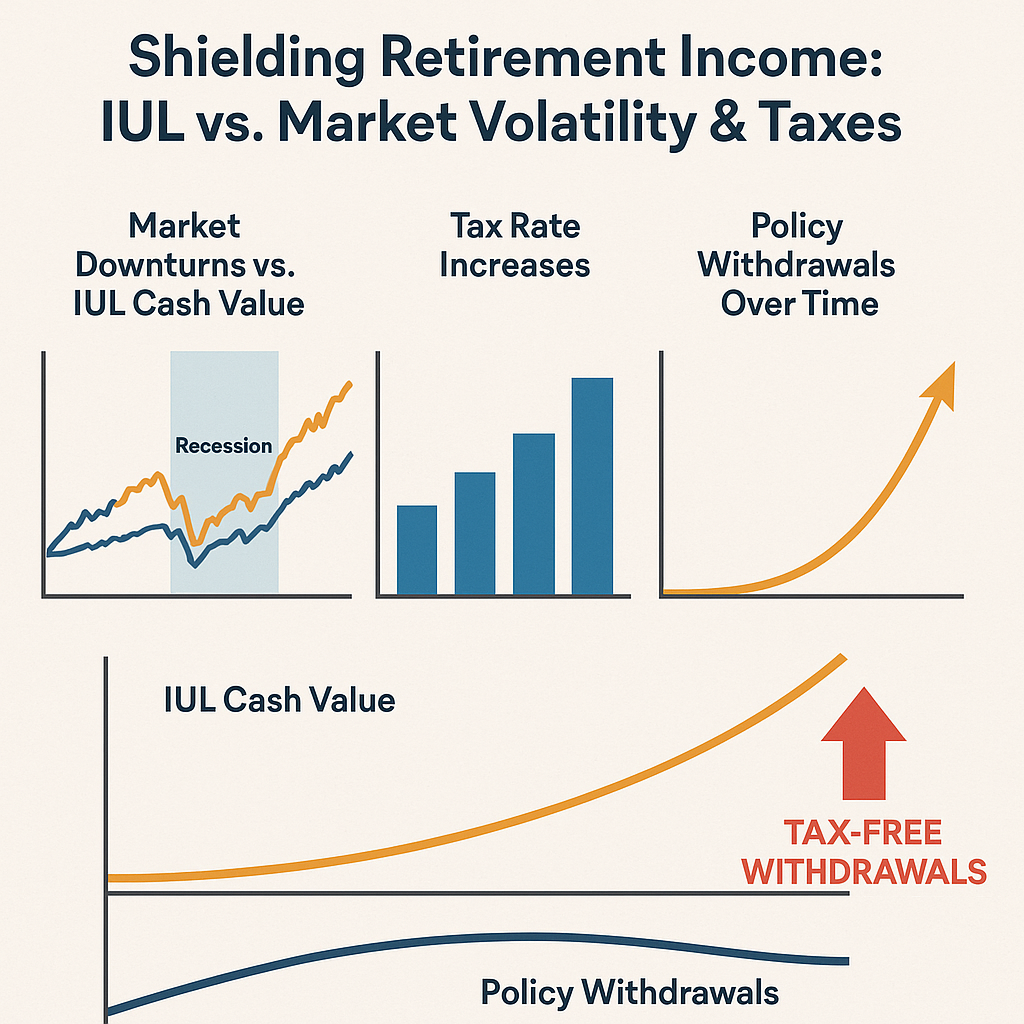

Hedging Against Taxes and Market Volatility

- No 59.5 withdrawal penalty: Unlike IRAs/401(k)s, you can access IUL cash value at any age[5].

- Protection from market downturns: IUL offers a 0% floor, ensuring you never lose principal due to market losses[4].

- Tax-exempt distributions: Strategic use of loans/withdrawals can shield distributions from rising taxes[5].

IUL for Over 55: Why This Age Group Is Especially Suited

- Peak earning years enable higher contributions.

- Retirement planning priorities: Need for tax-advantaged, flexible income sources.

- Estate planning urgency: Desire to transfer wealth efficiently.

- Long-term care risks: Opportunity to add riders for future protection[3].

According to AARP, nearly 70% of people turning age 65 will need some form of long-term care. Adding an LTC rider to IUL can help offset these costs.

Key Takeaways:

- People over 55 face unique financial transitions; IUL is designed to adapt to these needs.

Recent Updates: 2024 Tax Law Changes & Product Trends

- 2024 tax law changes: Increased estate tax exemption, changes to retirement account distributions, and new IRS guidance on life insurance cash value withdrawals.

- New IUL product riders: Enhanced long-term care, chronic illness, and accelerated death benefit riders introduced in 2024[3].

- Market trend: Growing preference for flexible, tax-advantaged products among retirees; IUL sales up 12% in 2024 (LIMRA).

Last updated: September 1, 2025

“Modern IUL products are more customizable than ever, allowing seniors to tailor coverage and riders to their specific retirement and health needs.” — John Carroll, Senior Vice President, LIMRA (2024)

[VIDEO SUGGESTION]

Title: “IUL for Retirees: 2024 Product Updates & Tax Changes”

Duration: 5-7 minutes

Key Points:

- 2024 tax law summary

- New IUL riders and options

- Real-world examples and testimonials

Interactive Tools for People Over 55

Retirement Income & IUL Benefit Calculator

Description:

A user-friendly calculator where people over 55 can enter their age, contribution amount, and desired retirement age to estimate:

- Projected cash value growth

- Tax-free annual income

- Death benefit at retirement

Purpose:

Empowers users to visualize IUL benefits tailored to their unique scenario.

Suitability Quiz: Is IUL Right for You After 55?

Description:

A guided questionnaire assessing:

- Retirement income goals

- Estate planning priorities

- Risk tolerance

- Need for long-term care coverage

Purpose:

Helps older adults determine if IUL aligns with their financial objectives and risk profile.

Frequently Asked Questions (FAQ)

What are the benefits of IUL for people over 55?

- Tax-deferred growth, tax-free withdrawals, flexible premiums, and customizable living benefits make IUL especially valuable for those nearing or in retirement.

How does IUL compare to other retirement options for seniors?

- IUL offers more flexibility and downside protection than whole life, term life, or annuities, and allows access to cash value without age penalties.

Are there risks to using IUL for retirement planning?

- Yes. Costs and complexity can be high, and policies may lapse if not managed properly. Work with a reputable advisor to design your plan.

Can I use IUL to fund long-term care?

- Yes. Many IUL policies offer riders that allow access to the death benefit for long-term care expenses.

Is the death benefit taxable?

- Generally, the death benefit is income-tax-free to beneficiaries.

Conclusion

Indexed Universal Life Insurance offers people over 55 a unique blend of flexibility, tax advantages, and living benefits that few other financial solutions can match. Whether you’re planning for retirement income, protecting your estate, or hedging against healthcare costs, IUL deserves careful consideration. Leverage interactive tools, consult with qualified advisors, and stay informed on the latest product features and tax laws to maximize your financial security in retirement.

References

[1]: Ogletree Financial – Tax Treatment of IUL Cash Value

[2]: Mutual of Omaha – The Power of IUL Video

[3]: Western & Southern – Indexed Universal Life Insurance

[4]: SmartAsset – Are IULs Worth It?

[5]: BankingTruths – Indexed Universal Life Insurance Pros & Cons

: NAIC – Life Insurance Basics

: AARP – Long-Term Care Statistics

: IRS – Life Insurance Guidance 2024

: LIMRA – Life Insurance Sales Trends

Author Bio:

William Noel is a Certified Financial Planner™ and licensed insurance advisor with over 20 years of experience helping older adults optimize retirement income and estate strategies. He holds the Chartered Life Underwriter (CLU) and Retirement Income Certified Professional (RICP) designations, and regularly contributes to national publications on insurance and retirement planning.